TL;DR:

- Travel insurance costs between 4% and 10% of prepaid, non-refundable trip expenses, depending on factors like age and coverage. Older travelers and international or high-risk trips incur higher premiums, with add-ons further increasing costs. Comparing quotes, matching coverage to actual needs, and considering existing benefits help travelers get the best value without overpaying.

Most travelers assume travel insurance is either cheap filler or an expensive luxury. The truth sits in between, and it’s more predictable than you’d think. What does travel insurance cost? For most trips, you’re looking at 4% to 10% of your total prepaid, non-refundable trip expenses. That means for a $5,000 vacation, expect to pay somewhere between $200 and $500. But your actual number depends on several factors that most travelers never think to check before buying. This guide breaks all of it down clearly so you can budget with confidence.

Table of Contents

- Key takeaways

- What does travel insurance cost on average?

- Factors that drive your premium up or down

- Domestic vs. international insurance costs

- How to get good value without overpaying

- My honest take on travel insurance pricing

- Plan your trip budget smarter with Pilottraveldeals

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Cost is a percentage, not a flat fee | Travel insurance typically runs 4% to 10% of your prepaid trip cost, scaling with trip price. |

| Age raises your premium significantly | Travelers over 60 pay considerably more; an 80-year-old pays an average of $628 more than a 20-year-old. |

| Add-ons can inflate premiums fast | Cancel For Any Reason coverage alone can increase your premium by up to 50% or more. |

| Domestic trips cost less to insure | Domestic policies average 3% to 8% of trip cost, while international coverage tends to run higher. |

| Comparing quotes is non-negotiable | Identical trips can yield wildly different quotes across providers, so always get multiple estimates. |

What does travel insurance cost on average?

The most reliable way to think about travel insurance cost is as a percentage of what you’ve already spent on your trip. Comprehensive plans cost between 4% and 10% of prepaid, non-refundable trip expenses for most travelers. That said, actual dollar amounts vary quite a bit based on the specific plan and traveler profile.

Here’s a practical look at how costs scale across different trip budgets in 2026:

| Trip Cost | Low Estimate (4%) | Mid Estimate (7%) | High Estimate (10%) |

|---|---|---|---|

| $1,000 | $40 | $70 | $100 |

| $2,500 | $100 | $175 | $250 |

| $5,000 | $200 | $350 | $500 |

| $10,000 | $400 | $700 | $1,000 |

For a $1,000 trip, insurance averages around 6% but can swing from as low as $40 to as high as $160 depending on the plan and your personal details. That’s a meaningful range, which is why plugging in your actual trip details matters more than using generic estimates.

Pro Tip: When calculating your insurable trip cost, only count prepaid, non-refundable expenses. Refundable hotel bookings don’t need to be included, which can actually lower your premium.

The average travel insurance price also depends on what the plan covers. A bare-bones trip cancellation policy costs far less than a full plan that includes medical coverage, emergency evacuation, and baggage protection. Knowing what you actually need before shopping prevents you from over-buying or under-protecting yourself.

Factors that drive your premium up or down

Understanding the factors affecting travel insurance cost gives you real leverage when shopping. These aren’t arbitrary pricing decisions. Each variable reflects actual risk that insurers are pricing into your policy.

Traveler age sits at the top of the list. Older travelers file more medical claims, so they pay more. An 80-year-old traveler pays an average of $628 more than a 20-year-old for comparable coverage. If you’re traveling with mixed-age groups, each person’s age affects the premium calculation for their portion of the trip.

Here are the other major pricing factors you need to know:

- Trip cost: The higher your non-refundable expenses, the more coverage you need and the more you’ll pay. Insurance scales proportionally.

- Trip length: A two-week international trip costs more to insure than a long weekend getaway. More days means more exposure to risk.

- Destination: Remote or high-risk destinations often carry higher premiums due to limited medical infrastructure and evacuation complexity.

- Coverage type: Medical-only plans are cheaper than all-inclusive plans. Trip cancellation coverage, baggage protection, and medical evacuation all add cost individually.

- Optional add-ons: Cancel For Any Reason (CFAR) coverage can increase your premium by around 50% on average. The range runs from 24% to 165% depending on the base plan.

- Number of travelers: Insuring a family of four costs more than covering a solo trip, though some family policies offer per-person discounts.

One factor people consistently overlook is their existing health insurance. If your domestic health plan provides some international coverage, you may be able to skip a standalone medical plan and buy a more targeted policy instead. This can shave real money off your total cost.

Pro Tip: Check whether your credit card includes any travel insurance benefits before you buy a separate policy. Some premium travel cards cover trip cancellation or lost baggage up to a certain limit, reducing what you need to purchase.

For a deeper look at how different policy types match different trip scenarios, the types of travel insurance guide at Pilottraveldeals walks through your main options clearly.

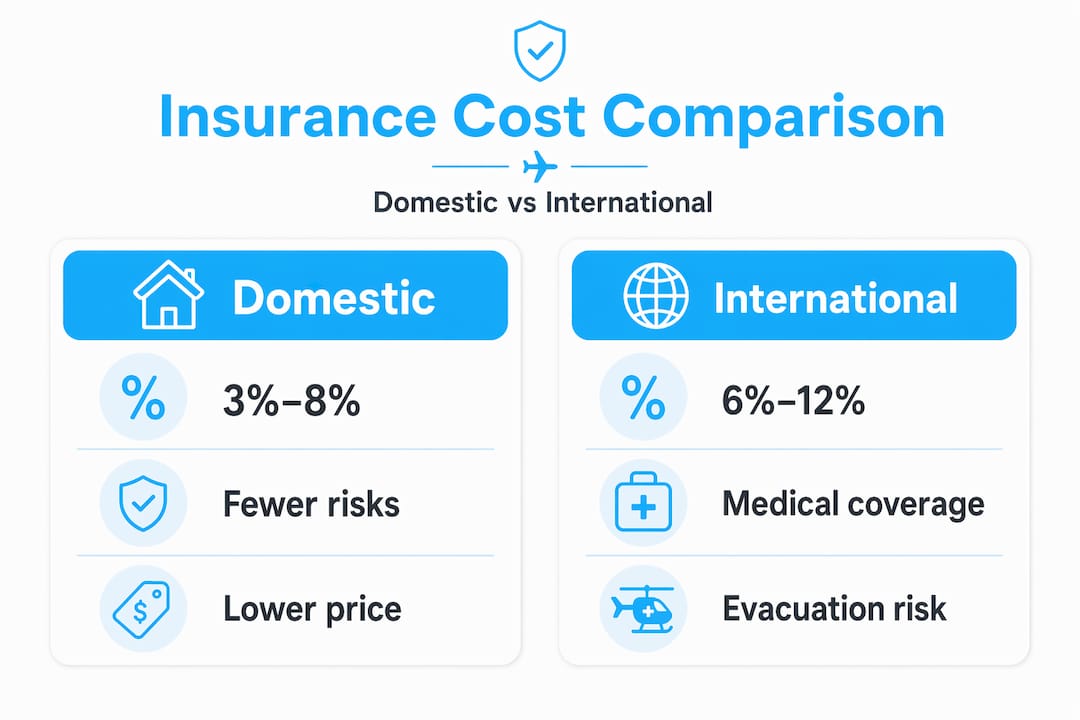

Domestic vs. international insurance costs

Here’s a misconception that costs travelers real money. Many travelers expect domestic and international coverage to cost about the same. They don’t, and the gap is significant.

Domestic travel insurance typically runs 3% to 8% of trip cost, sitting at the lower end of the general range. International coverage often pushes toward the higher end because of the added risk of medical care abroad. Emergency medical evacuation from a remote international location can cost tens of thousands of dollars, a risk that insurers price directly into international policies.

| Coverage Type | Typical Cost Range | Key Risk Factor |

|---|---|---|

| Domestic travel | 3% to 8% of trip cost | Simpler logistics, lower evacuation costs |

| International travel (developed country) | 5% to 9% of trip cost | Higher medical costs, currency risk |

| International travel (developing country) | 7% to 12% of trip cost | Limited medical infrastructure, evacuation complexity |

| Adventure or high-risk destination | 10%+ of trip cost | Specialized medical needs, extreme sports coverage |

If you’re flying within the United States and your health insurance follows you across state lines, the case for comprehensive travel medical coverage weakens. What you probably still need is trip cancellation and interruption coverage, since domestic flights get canceled and hotels don’t always refund last-minute changes.

For international trips, prioritize medical coverage and evacuation. A European vacation to a country with strong healthcare infrastructure carries less medical risk than a trip to a rural destination with limited hospital access. Adjusting your coverage to match your actual destination is one of the smartest ways to manage the cost of travel insurance without sacrificing real protection.

How to get good value without overpaying

Getting good value on travel insurance isn’t about finding the cheapest price. It’s about matching coverage to what you actually need, then finding the best price for that coverage. Here’s how to do it:

-

Start with your trip’s actual risk profile. A refundable weekend trip needs less coverage than a $12,000 international tour with prepaid hotels and excursions. Know what you’re protecting before you shop.

-

Get at least three quotes. Pricing for identical trips varies significantly between providers. The same traveler with the same trip details can see quotes differ by 50% or more. Use a comparison platform to see multiple options side by side.

-

Match coverage limits to actual expenses. Buying $10,000 in trip cancellation coverage for a $3,000 trip wastes money. Only insure what you’d actually lose.

-

Skip add-ons you won’t use. CFAR coverage sounds appealing, but it adds roughly 50% to your premium. Unless you have a genuine reason to cancel that wouldn’t be covered by standard trip cancellation, you’re paying for flexibility you probably won’t need.

-

Consider an annual policy if you travel frequently. Annual travel insurance plans can offer real savings for travelers who take three or more trips per year. The per-trip cost typically drops substantially compared to buying individual policies each time.

-

Read the exclusions before you buy. Pre-existing medical condition clauses, extreme sports exclusions, and specific destination restrictions can void coverage. A cheap plan that won’t pay out isn’t actually cheap.

-

Buy early. Purchasing travel insurance shortly after your first trip payment locks in pre-existing condition waivers and often CFAR eligibility. Waiting until the week before departure limits your options and sometimes increases cost.

For practical strategies on finding affordable coverage, Pilottraveldeals has a focused guide that covers the comparison process step by step. Understanding why travel insurance matters for budget-focused trips is also worth reading before you finalize your plan.

My honest take on travel insurance pricing

I’ve helped a lot of travelers think through their trip budgets over the years, and travel insurance pricing is where I see the most consistent confusion. People either dismiss it as too expensive without actually running the numbers, or they buy whatever the airline checkout page offers without comparing alternatives.

The airline add-on problem is real. Those checkout-page policies are almost always overpriced for what they cover. I’ve seen travelers pay 15% of their trip cost through an airline upsell when an equivalent or better policy was available for 6% through a dedicated insurer. That difference on a $4,000 trip is $360 in your pocket.

What I’ve learned watching travelers navigate this is that the primary cost drivers including trip cost, age, trip length, and coverage limits, are all things you can influence. You can choose trip lengths, you can select refundable bookings to reduce your insurable base, and you can prioritize coverage types based on real risk rather than theoretical worst-case scenarios.

The age factor surprises people most. A couple where one partner is 68 and the other is 32 will see very different individual premiums. Planning for that in advance rather than discovering it at checkout makes the budgeting conversation much more productive.

My honest recommendation: treat travel insurance as a line item in your trip budget from day one, not an afterthought. Budget 7% of your non-refundable expenses and adjust from there once you’ve compared actual quotes. That number won’t be perfect for every trip, but it gives you a working target that holds up across most traveler profiles and destination types.

— Asher

Plan your trip budget smarter with Pilottraveldeals

Knowing what travel insurance costs is just one piece of the trip budget puzzle. When you’re managing flights, hotels, and activities alongside insurance premiums, every dollar you save somewhere else gives you more flexibility to get the coverage you actually need.

Pilottraveldeals exists exactly for this kind of budget balancing act. The platform compares deals across flights, hotels, and travel services so you can see your full trip cost picture in one place. When you save on hotel bookings or lock in lower airfare, you free up budget for proper insurance coverage rather than cutting corners on protection. International travelers can also reduce trip costs by planning around travel SIM cards instead of costly roaming fees. Use Pilottraveldeals to get your core trip costs under control, then allocate the savings toward coverage that actually protects your investment.

FAQ

How much does travel insurance cost on average?

Travel insurance typically costs between 4% and 10% of your total prepaid, non-refundable trip expenses. For a $5,000 trip, that puts the average range at $200 to $500.

Does traveler age affect the cost of travel insurance?

Yes, significantly. Older travelers pay higher premiums due to increased medical risk, with an 80-year-old averaging $628 more than a 20-year-old for similar coverage.

Is international travel insurance more expensive than domestic?

Yes. Domestic policies generally cost 3% to 8% of trip cost, while international coverage runs higher due to medical evacuation risks and limited healthcare access in some destinations.

What is Cancel For Any Reason coverage and how much does it add?

CFAR is an optional add-on that lets you cancel for reasons not covered by standard policies. It typically increases your premium by around 50%, though the range can stretch from 24% to over 165%.

When does an annual travel insurance policy make more sense?

Annual policies tend to be cost-effective if you take three or more trips per year. The per-trip cost drops considerably compared to buying individual policies for each journey, though coverage limits per trip may differ from single-trip plans.

Recommended

- Why buy travel insurance: protect budget trips 2026 – PilotTravelDeals.com

- Find the cheapest travel insurance for smart, budget trips – PilotTravelDeals.com

- Cheap international flight tickets: save more in 2026 – PilotTravelDeals.com

- Mistakes to Avoid When Booking Travel in 2026 – PilotTravelDeals.com