TL;DR:

- TD travel medical insurance covers emergency medical expenses incurred abroad, excluding routine and elective care. It offers single-trip and multi-trip plans, with costs influenced mainly by age, destination, trip length, and existing TD relationships. Travelers should understand sub-limits like dental and paramedical caps, which often limit actual reimbursements despite high headline coverage.

TD travel medical insurance is defined as a policy that covers eligible emergency medical expenses incurred while traveling outside your home province or territory in Canada. The standard industry term is “travel health insurance,” and TD Insurance offers it under that umbrella alongside broader travel protection products. With coverage up to $10 million per insured person, TD’s plans are built for the reality that a single medical emergency abroad can generate bills that dwarf the cost of the trip itself. This guide breaks down exactly what TD covers, how plans differ, what drives the price, and how to buy the right policy before you leave.

What does TD travel medical insurance cover?

TD travel medical insurance covers emergency medical treatment that becomes necessary while you are outside your home province or territory. The core benefit categories are hospital stays, physician fees, ambulance transport, diagnostic services like X-rays and lab work, prescription drugs, and medical appliances. These are the expenses that can spiral fastest in destinations like the United States, where a single emergency room visit routinely costs thousands of dollars.

Beyond the headline medical benefits, the plan extends to several supporting categories that travelers frequently overlook:

- Emergency dental treatment: Covered up to $2,000 per insured person for accidental dental injuries or sudden dental pain.

- Meals and lodging: If a medical emergency delays your return home, TD covers incidentals up to $1,500 so you are not paying out of pocket for a hotel while you recover.

- Paramedical services: Covered up to $300 per profession, which applies to services like physiotherapy or chiropractic care required as part of emergency treatment.

- Medical appliances: Crutches, casts, and similar devices prescribed during an emergency are included.

What is not covered matters as much as what is. TD travel medical insurance excludes pre-existing conditions unless they are specifically addressed in the policy, and it does not cover routine checkups, planned procedures, or elective surgeries. If you book a trip knowing you will need a medical procedure abroad, that cost falls entirely on you.

Understanding these exclusions upfront prevents the most common source of claim disputes. Travel health coverage is emergency-only protection, not a substitute for your provincial health plan or a way to access cheaper medical care abroad.

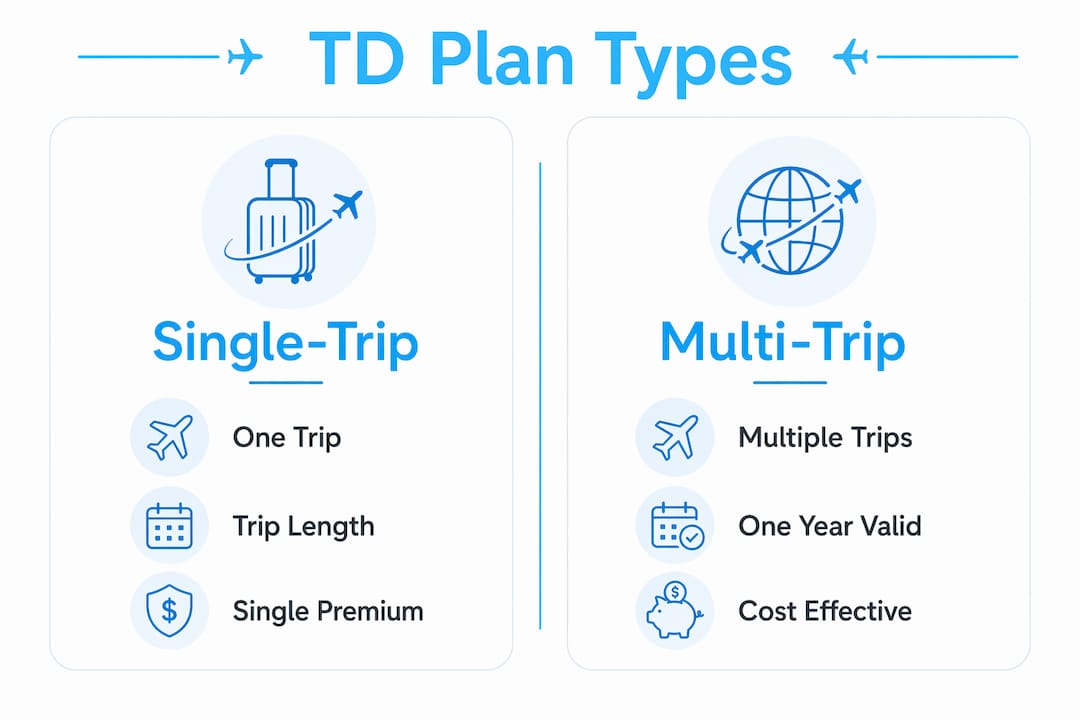

How do TD travel medical insurance plans differ?

TD offers two primary plan structures: single-trip and multi-trip. Choosing between them depends almost entirely on how often you travel outside your province in a given year.

| Plan type | Best for | Key feature |

|---|---|---|

| Single-trip | One international trip per year | Covers one journey; priced per trip length |

| Multi-trip | Frequent travelers (2+ trips/year) | Annual plan covering multiple trips |

| Top-up/extension | Travelers extending a trip | Adds coverage days to an existing plan |

| Trip cancellation add-on | Any traveler with prepaid costs | Reimburses non-refundable expenses if you cancel |

Single-trip plans cover one journey outside your home province or territory and are priced based on trip length, destination, and traveler profile. Multi-trip plans suit frequent travelers because they remove the administrative burden of buying a new policy before every departure. The trade-off is that switching plan structures mid-year typically requires purchasing a new policy entirely, so choosing the right structure at the start of the year matters.

TD also offers family and couple plan options, which cover up to six people under a single premium. For families traveling together, this is almost always more cost-effective than buying individual policies. Add-ons like trip cancellation and interruption coverage can be layered onto a medical plan, giving you a more complete protection package without buying a separate product from a different provider.

Pro Tip: If you take more than two trips outside your province per year, run the numbers on a multi-trip plan before defaulting to single-trip. The per-trip savings often cover the cost difference within the first two journeys.

For a broader look at how travel medical fits alongside other protection products, the types of travel insurance guide at Pilottraveldeals is a useful starting point.

What factors influence the cost of TD travel medical insurance?

Four variables drive the premium on any TD travel health insurance plan: your age, your health status, the length of your trip, and your destination.

- Age is the single largest cost driver. Older travelers represent higher statistical risk for emergency medical events, so premiums rise significantly after age 60.

- Trip length scales the premium directly. A 30-day trip costs more to insure than a 7-day trip because the exposure window is longer.

- Destination affects pricing because medical costs vary dramatically by country. Traveling to the United States costs more to insure than traveling to most of Europe or Southeast Asia.

- Existing TD customer status can unlock discounts. TD Insurance offers reduced rates for customers who already hold other TD products.

To put real numbers to this: sample premiums for a 7-day trip start around $40 for a 25-year-old solo traveler and reach approximately $86 for a family of up to six. That gap illustrates how efficiently family plans distribute the per-person cost. For budget-conscious travelers, understanding how to find affordable travel insurance options can help you balance coverage quality against premium cost.

Timing also affects your options, if not always the base premium. Trip cancellation and interruption coverage can be added up to 186 days before departure, but purchasing it early locks in protection from the moment you make your first trip payment. Waiting until the week before you fly eliminates that early-purchase benefit entirely.

How to choose and buy the right plan for your trip

Selecting the right TD travel insurance option comes down to matching the policy’s terms to the specific details of your trip. Generic advice to “buy travel insurance” misses the practical steps that prevent coverage gaps.

Start with these checks before you purchase:

- Confirm your travel dates trigger the policy. TD travel medical insurance activates when you leave your home province or territory. A road trip that crosses a provincial border qualifies; a flight that connects through another Canadian city before going international also qualifies. Verify that your travel dates and destinations match the policy’s outside-province requirement precisely.

- Read the policy document, not just the summary. Marketing summaries highlight the $10 million headline limit. The policy document contains the sub-limits, exclusion clauses, and definitions that determine whether your specific claim gets paid.

- Match coverage limits to destination risk. A trip to the United States warrants maximum coverage because American hospital costs are the highest in the world. A trip to a country with universal healthcare and lower medical costs may allow for a lower coverage tier.

- Buy before your first trip payment, not before your departure date. Purchasing early activates cancellation and interruption benefits from day one of your booking window.

- Use TD’s official resources as your primary reference. TD Insurance’s official content provides accurate plan specifications. Third-party summaries sometimes lag behind policy updates and can misrepresent coverage details.

Pro Tip: Before finalizing any plan, write down the three most likely medical scenarios for your specific trip, a sprained ankle on a hiking trip, a stomach illness in a developing country, or a dental emergency, and check whether each one falls within the covered categories and sub-limits.

For travelers heading abroad, pairing solid travel health coverage with a practical safety checklist reduces both financial and physical risk significantly.

Key takeaways

TD travel medical insurance provides the strongest protection when you understand both the headline limits and the sub-limits that govern real-world claims.

| Point | Details |

|---|---|

| Coverage scope | Emergency medical expenses only; routine and elective care are excluded from all standard plans. |

| Sub-limits matter | Dental ($2,000), meals and lodging ($1,500), and paramedical ($300) caps affect actual reimbursement more than the $10 million headline limit. |

| Plan structure choice | Single-trip suits occasional travelers; multi-trip plans save time and money for those taking two or more trips per year. |

| Cost drivers | Age, destination, trip length, and TD customer status are the four main variables that determine your premium. |

| Buy early | Purchasing before your first trip payment activates cancellation benefits; waiting until departure eliminates that protection window. |

Why sub-limits deserve more attention than the headline number

Most travelers I speak with fixate on the $10 million coverage limit and stop reading there. That number is reassuring, and it should be. But in practice, the claims that create the most friction are not the catastrophic ones. They are the mid-range emergencies where sub-limits become the binding constraint.

Consider a traveler who slips on a hiking trail in Costa Rica, fractures a wrist, and needs emergency physiotherapy alongside the orthopedic treatment. The hospital bill may fall well within the $10 million ceiling, but the paramedical sub-limit of $300 per profession caps the physiotherapy reimbursement at a fraction of the actual cost. That gap comes out of your pocket, not TD’s.

The same logic applies to emergency dental. A $2,000 dental sub-limit sounds generous until you price an emergency root canal in the United States, where the procedure alone can exceed that figure. Travelers heading to high-cost destinations should factor these caps into their planning, not just the headline number.

My honest recommendation: treat the sub-limits as the real coverage floor and the $10 million as the ceiling for catastrophic events. If the sub-limits feel too low for your destination or activity profile, ask about supplemental coverage or consider whether a higher-tier plan addresses those gaps. Consulting a licensed insurance professional before purchasing is worth the time, particularly for travelers with complex health histories or high-risk itineraries. The why buy travel insurance resource at Pilottraveldeals also frames the financial case clearly for travelers who are still on the fence.

— Asher

Plan your trip smarter with Pilottraveldeals

Protecting yourself with solid travel health coverage is one half of smart trip planning. The other half is making sure you are not overpaying for flights and hotels. Pilottraveldeals compares deals across airlines and hotel providers, with savings that regularly reach up to 80% off standard rates. Whether you are booking a quick weekend trip across the border or a month-long international adventure, finding the right hotel deals before you go frees up budget that can offset your insurance premium entirely. Check out Pilottraveldeals for cheap airfare tips and hotel comparisons to build a trip that is both well-protected and well-priced.

FAQ

What is TD travel medical insurance?

TD travel medical insurance is a travel health policy that covers eligible emergency medical expenses incurred outside your home province or territory in Canada. It is not a substitute for provincial health coverage but a supplement for emergencies that occur while traveling abroad.

Does TD travel medical insurance cover pre-existing conditions?

Standard TD travel medical insurance excludes pre-existing conditions unless the policy specifically includes them. Travelers with chronic conditions should review the policy terms carefully or ask about plans that offer pre-existing condition coverage.

How much does a TD single-trip medical plan cost?

Premiums start around $40 for a 25-year-old on a 7-day trip and reach approximately $86 for a family of up to six. Age, destination, and trip length are the primary variables that move the price up or down.

When should I buy TD travel medical insurance?

Purchase your plan before making your first trip payment, not just before departure. Buying early activates trip cancellation and interruption benefits from the moment you book, and cancellation coverage can be added up to 186 days before your departure date.

Is a multi-trip plan better than a single-trip plan?

A multi-trip plan is the better choice if you travel outside your province more than twice a year. Switching plan structures mid-year requires buying a new policy, so choosing the right structure at the outset saves both money and administrative effort.

Recommended

- 5 Types of Travel Insurance: Options for Every Traveler – PilotTravelDeals.com

- What Does Travel Insurance Cost in 2026? – PilotTravelDeals.com

- Find the cheapest travel insurance for smart, budget trips – PilotTravelDeals.com

- Travel safety checklist: practical tips for budget 2026 – PilotTravelDeals.com

{kind=link}