TL;DR:

- The best airline credit card depends on individual travel habits, loyalty, and perks valued. Co-branded cards suit loyal airline travelers, while flexible cards offer broader redemption options and protection against devaluations. Combining both types with organized management maximizes travel benefits and savings.

If you’ve ever searched for what airline has the best credit card and walked away more confused than when you started, you’re not alone. The honest answer is that no single card wins for every traveler. The right card depends on where you fly, how often you check bags, whether you’re loyal to one airline, and how much complexity you’re willing to manage. This guide cuts through the noise and breaks down the best airline credit card offers of 2026 so you can make a decision that actually fits your travel life.

Table of Contents

- Key takeaways

- What airline has the best credit card for your travel style?

- Top co-branded airline cards of 2026

- Flexible travel cards worth knowing

- How to pick the right card for you

- My honest take on chasing the “best” card

- Put your card strategy to work with Pilottraveldeals

- FAQ

Key takeaways

| Point | Details |

|---|---|

| No universal best card | The best airline card depends on your travel frequency, loyalty, and how you value specific perks. |

| Co-branded vs. flexible | Co-branded cards reward loyal flyers; flexible cards protect you from devaluations and suit multi-airline travelers. |

| Bag savings drive real value | Free checked bags alone can justify most airline card annual fees for families flying 3+ times a year. |

| Hybrid wallets win | Pairing a flexible points card with a co-branded card gives you the widest coverage of perks and flexibility. |

| Activate or lose | High-fee cards like the Amex Platinum only pay off when you actively track and use layered monthly credits. |

What airline has the best credit card for your travel style?

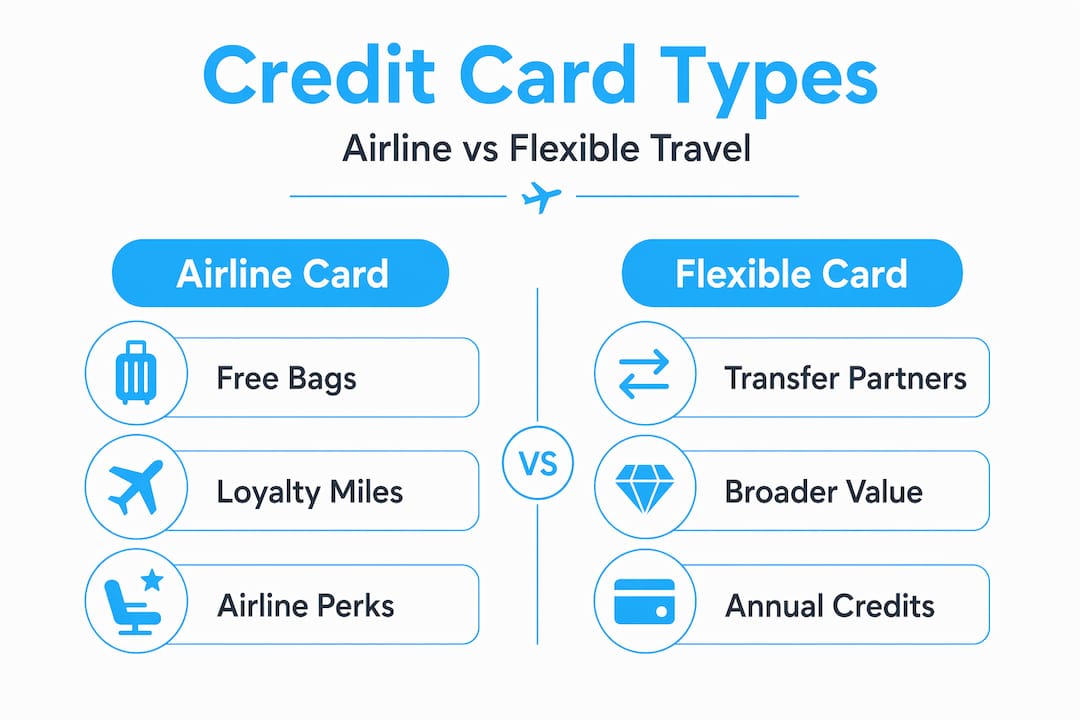

Before comparing specific cards, you need to understand the two categories they fall into. Getting this distinction right is more valuable than any single card recommendation.

Co-branded airline cards are issued in partnership with a specific airline. You earn miles in that airline’s loyalty program, and the perks are tailored to that carrier: free checked bags, priority boarding, discounted companion fares, and an accelerated path toward elite status. The catch is that your rewards are locked into one ecosystem. If that airline cuts routes, raises award prices, or devalues its miles, your points take the hit too.

Flexible travel credit cards earn points in a bank’s own rewards currency, like Chase Ultimate Rewards, Amex Membership Rewards, or Capital One Miles. You can transfer those points to a dozen or more airline and hotel partners. The trade-off is fewer airline-specific perks, like no free bags on a specific carrier, but far more control over where and how you redeem.

Here is how to think about which type fits you:

- You fly one airline more than 80% of the time and check bags regularly. Go co-branded.

- You book whoever has the cheapest fare and switch airlines by season or destination. Go flexible.

- You travel frequently for both work and leisure. Consider holding both types.

Pro Tip: Flexible travel points are a natural hedge against devaluation risk. Emirates Skywards raised award costs in May 2026, and travelers locked into those miles had no escape hatch.

Top co-branded airline cards of 2026

Airline-specific cards vary more than most people realize. Annual fees, bag policies, and bonus structures differ enough that the wrong card can cost you money instead of saving it.

| Card | Annual Fee | Signup Bonus | Free Bags | Best For |

|---|---|---|---|---|

| JetBlue Plus Card | $99 | 70,000 points | Cardholder + 3 companions | East Coast and Florida families |

| Southwest Premier | $149 | Varies | 2 bags, all companions | Domestic loyalists chasing Companion Pass |

| Delta SkyMiles Gold | $150 | 40,000–70,000 miles | Cardholder only | Casual Delta flyers |

| United Explorer | $95 | 50,000–60,000 miles | Cardholder + 1 companion | Moderate United travelers |

| Citi Strata Premier | $95 | 75,000 points | Via American perks | Heavy AA flyers earning 3x categories |

The JetBlue Plus Card stands out for families. The free checked bags for the cardholder plus up to three companions can generate $1,800 to $2,800 in annual value for a family flying JetBlue four or more times a year, well beyond the $99 annual fee.

The Southwest Premier is one of the most underrated cards in the domestic market. The Companion Pass and free bags generate $1,300 to $1,900 in annual value for frequent Southwest travelers who take multiple trips per year.

For American Airlines flyers, the Citi Strata Premier earns 3x points across multiple categories including hotels, rentals, and transit, plus up to $700 in annual credits. The premium Citi Strata Elite tier adds Priority Pass lounge access and hotel credits worth hundreds of dollars per year.

Pro Tip: Before applying for any co-branded card, calculate your average annual bag fees first. If you check two bags roundtrip on four flights a year, you’re already spending $400 or more. That math alone often justifies the annual fee.

One more important point: mid-fee airline cards like Delta SkyMiles Gold and United Explorer are the sweet spot for semi-frequent travelers. They deliver solid starter perks without burying you in credits and activations you’ll forget to use.

Flexible travel cards worth knowing

If you’re asking what is the best flight credit card across multiple airlines, the answer usually lives in the flexible points world. These cards are better at protecting your rewards long-term and giving you options when award availability is tight.

Here are the four cards that consistently rank at the top of the airline credit card comparison for flexibility:

- Chase Sapphire Reserve: $550 annual fee, $300 travel credit, Priority Pass lounge access, 3x on dining and travel, transfer partners include United, Southwest, British Airways, and Air France/KLM.

- Chase Sapphire Preferred: $95 annual fee, $50 hotel credit, 2x on travel and dining, same transfer partner list. The best entry-level flexible card available.

- Capital One Venture X: $395 annual fee with $300 annual travel credit and 10,000 bonus miles each anniversary. Transfers to Air Canada, Turkish Airlines, and others.

- American Express Platinum: $695 annual fee, but over $3,000 in annual value is achievable if you actively use the layered credits for travel, dining, entertainment, and airline incidentals.

The Amex Platinum is worth a longer look because it confuses a lot of people. The $695 fee looks alarming until you realize the credits are spread monthly, quarterly, and semiannually. Active benefit management is the difference between getting crushed by the fee and coming out far ahead.

Pro Tip: Create a calendar reminder for every benefit reset date on high-fee cards. Losing a $20 monthly Uber credit three months in a row because you forgot to activate it adds up to $60 in the garbage. These cards reward the organized traveler.

You can also extend your points further by learning how international airline programs work as transfer partners. Transferring Chase points to Air France/KLM Flying Blue for a short-haul European flight can cost a fraction of what you would pay in dollars.

How to pick the right card for you

No airline credit card comparison is useful unless you apply it to your own situation. Here is a practical framework to narrow your choice.

- Identify your primary airline. If you fly one carrier for more than half your trips, a co-branded card immediately makes sense. If you buy the cheapest fare available, a flexible card wins.

- Count your checked bags. Bag fee savings are the fastest way to justify an annual fee. One roundtrip with two bags at a major carrier costs $70 to $100. Run the numbers against your annual fee.

- Assess your companion travel. Cards like JetBlue Plus and Southwest Premier extend free bags to companions. If you travel with family or a partner, this multiplies the value dramatically.

- Decide how much complexity you will actually manage. A $695 card is a great deal on paper and a bad deal in practice if you’re not the type to track quarterly credits and activate offers.

- Consider lounge access honestly. Premium cards often justify their fees through lounge access alone for frequent travelers. But if you fly six times a year, you may not visit a lounge enough to make it matter.

- Think about a hybrid wallet. Advanced travelers often hold a premium flexible card plus one co-branded card. The flexible card handles points earning and lounge access while the co-branded card covers free bags and status on a preferred airline.

Pro Tip: Use airline alliances to stretch your co-branded card further. Miles on United, for example, can book Star Alliance partner flights, sometimes at lower award prices than United itself charges.

Understanding how to maximize travel discounts beyond just credit cards adds another layer to this strategy. The best travelers combine card perks with smart booking timing, not just one or the other.

My honest take on chasing the “best” card

I’ve spent years watching travelers fall into the same trap. They read a headline calling some card the “best airline credit card” and apply without checking whether they even fly that airline more than twice a year. The card sits in their wallet earning mediocre rewards, and the annual fee renews without a second thought.

In my experience, the best strategy isn’t one card. It’s a deliberate combination. I hold a flexible points card as my primary earner because transferable points give me real protection when an airline program devalues overnight. I pair it with one co-branded card for the airline I use most, specifically for the free bags and priority boarding that make a real difference on travel days.

What I’ve learned is that most people overestimate how much they’ll use premium perks and underestimate how much they’ll benefit from something as unglamorous as a free checked bag. A family of four getting free bags on six JetBlue flights a year is saving real money. A solo traveler paying $695 for a card they rarely use is just paying $695.

Review your card portfolio at least once a year. Airlines change their programs, annual fees shift, and your own travel patterns evolve. What made sense in 2024 may not be the right fit today.

— Asher

Put your card strategy to work with Pilottraveldeals

Your credit card is only half the equation. The other half is knowing where to book.

At Pilottraveldeals, we track deals across airlines, hotels, and travel services so you can stack your card rewards on top of already-discounted fares and accommodations. Pairing a strong airline card with a platform that surfaces the best prices is where real savings happen. Check out our cheap airfare tips to see how to time your bookings for maximum value, and browse our hotel deals to stretch those flexible points even further. Whether you’re a loyalist earning elite status or a bargain hunter mixing and matching airlines, the right booking strategy makes your rewards go significantly further than the card alone ever could.

FAQ

What airline has the best credit card overall?

There is no single best card for every traveler. JetBlue Plus is exceptional for families, Southwest Premier for domestic loyalists, and Citi Strata for heavy American Airlines flyers.

What is the best airline credit card for families?

The JetBlue Plus Card covers free bags for up to 3 companions, making it one of the highest-value cards for families flying together multiple times a year.

Are flexible travel cards better than co-branded airline cards?

Flexible cards offer broader value and protection from program devaluations, but co-branded cards deliver better targeted perks for loyal airline customers. The best approach often combines both.

What is the best flight credit card for beginners?

The Chase Sapphire Preferred at $95 per year is widely considered the top entry point. It earns transferable points, covers travel broadly, and has the same airline transfer partners as far more expensive cards.

How many airline credit cards should I hold?

Most travelers do well with one to two cards. A hybrid wallet approach pairing a flexible card with one co-branded card covers the majority of travel scenarios without creating complexity that leads to wasted fees.

Recommended

- Cheap Airline Benefits That Savvy Travelers Actually Use – PilotTravelDeals.com

- Airline Alliances Explained: Maximizing Travel Savings – PilotTravelDeals.com

- Unlock more value with international airline programs – PilotTravelDeals.com

- What is travel credit? A 2026 guide for budget travelers – PilotTravelDeals.com