TL;DR:

- Affordable travel insurance can provide good value if it covers your specific needs and risks.

- While the cheapest plans often have coverage gaps, spending slightly more can protect you from costly emergencies in remote or high-cost destinations.

Not all cheap travel insurance is created equal, and the good news is that “affordable” doesn’t automatically mean “useless.” Based on analysis of over 10,000 quotes, Tin Leg consistently offers the lowest-priced plans on the market, which proves that bargain options from reputable carriers genuinely exist. But finding the right one for your specific trip takes a little more than just grabbing the lowest number on the screen. This guide breaks down exactly what makes a plan cheap, which providers deliver the best value, what trade-offs you need to accept, and how to pick the smartest policy for every dollar you spend.

Table of Contents

- What actually makes travel insurance ‘cheap’?

- Top cheap travel insurance providers compared

- What risks and gaps come with the cheapest plans?

- How to choose the right cheap insurance for your trip

- Why focusing only on the lowest price can backfire for travelers

- Find more ways to save on travel essentials

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| No one-size-fits-all | Cheapest plans vary by age, trip, and destination, so comparison is key. |

| Coverage matters most | Focusing only on price can leave you underinsured for emergencies. |

| Top picks for savings | Tin Leg, Trawick International, and Berkshire Hathaway consistently offer affordable plans. |

| Watch for hidden limits | Inexpensive plans may exclude essential coverages or set low medical caps. |

| Buy early for best value | Purchasing shortly after booking increases eligibility for valuable policy benefits. |

What actually makes travel insurance ‘cheap’?

The word “cheap” gets thrown around a lot, but it rarely means the same thing twice. When it comes to travel insurance, price is not a fixed number. It shifts based on a wide range of personal and trip-specific factors, which is why comparison shopping matters so much.

Here’s what directly affects how much you pay:

- Your age. Older travelers pay significantly more because they present a higher medical risk to insurers.

- Your destination. International trips, especially to remote or high-cost medical regions, cost more to insure than domestic ones.

- Trip length. A 10-day international vacation costs more to cover than a 3-day weekend getaway.

- Total trip cost. Policies often cover a percentage of your prepaid, nonrefundable expenses, so more expensive trips cost more to insure.

- Coverage type. Basic plans with limited medical caps are cheaper than comprehensive plans with higher limits, cancel-for-any-reason (CFAR) add-ons, and primary medical coverage.

There is no universally cheapest plan because cost depends entirely on age, destination, and trip length. A plan that’s the cheapest option for a 28-year-old taking a four-day domestic trip could be one of the more expensive ones for a 62-year-old heading to Southeast Asia for three weeks.

“The lowest premium is only a good deal if the plan actually covers what could go wrong on your specific trip.”

The real trap many budget travelers fall into is treating price as the only filter. A $25 policy sounds amazing until you realize it caps emergency medical coverage at $10,000, which won’t even cover two nights in a foreign hospital. Understanding why budget travelers need insurance in the first place helps frame what “good cheap” actually looks like versus what’s just a low number with a lot of fine print.

There are also moments when spending slightly more is the smarter budget move. If your trip involves adventure sports, pre-existing medical conditions, or international destinations with high healthcare costs, upgrading from a $43 basic plan to a $61 comprehensive plan could save you thousands in an emergency. Exploring the full range of travel insurance options helps you understand exactly what those upgrades buy you.

Pro Tip: Always get at least three quotes for the same trip details before committing to a plan. The same destination, trip length, and coverage level can vary by 40% or more across providers.

Top cheap travel insurance providers compared

After understanding what affects price, let’s look at which brands consistently deliver the lowest-cost options in real-world scenarios. Not all affordable insurers are equally reliable, and a few names keep rising to the top of independent analyses.

US News ranks Trawick International, Tin Leg, and Berkshire Hathaway among the most affordable travel insurance companies for 2026. These aren’t fringe brands, either. They’re well-capitalized, licensed carriers with real claims-paying ability.

Here’s a direct comparison of the major budget-friendly providers:

| Provider | Basic plan cost | Comprehensive plan cost | Medical coverage (basic) | Best for |

|---|---|---|---|---|

| Tin Leg | $43 (lowest basic) | $61 (cheapest comprehensive) | $50,000 | Short and domestic trips |

| Travelex Essential | $25 to $60 est. | $80 to $120 est. | $50,000 | Families and simple trips |

| Seven Corners | $81 basic | $120 to $150 est. | $100,000 | Mid-range coverage seekers |

| World Nomads Standard | $81 standard | $130 to $170 est. | $100,000 | Adventure travelers under 65 |

| Trawick International | $55 to $70 est. | $90 to $130 est. | $150,000 | International budget travelers |

Tin Leg leads on price at both the basic and comprehensive levels. Their basic plan at $43 is the lowest priced basic plan available based on broad market analysis, while their Platinum plan at $61 holds the title of cheapest comprehensive option. That’s a significant value gap compared to providers like Seven Corners and World Nomads, which come in nearly double the price for a comparable starting plan.

What do the cheapest plans typically exclude? Here are the most common omissions at the lowest price tier:

- Cancel for any reason (CFAR) coverage

- Pre-existing condition waivers (unless purchased within 14 to 21 days of booking)

- Primary medical coverage (most use secondary, meaning your own health insurance pays first)

- High emergency evacuation limits (often capped at $100,000 or less)

- Coverage for extreme or adventure sports

- “Interruption for any reason” upgrades

For travelers hunting the best sites for budget deals across flights, hotels, and insurance in one place, knowing which provider matches your trip type saves both time and money.

Pro Tip: Tin Leg’s Platinum plan at $61 is one of the most competitive comprehensive options on the market. If your trip is international, the $18 jump from basic to Platinum is almost always worth it.

What risks and gaps come with the cheapest plans?

Even the best cheap plans have real trade-offs. Knowing exactly what you might be giving up helps you decide whether the savings are worth it or whether a slightly higher premium makes more financial sense.

The biggest gaps in low-cost travel insurance fall into these categories:

- Low medical coverage caps. Many basic plans cap medical coverage at $50,000. A single serious accident abroad, especially in countries like Japan, Australia, or the United States if you’re a foreign visitor, can generate bills far exceeding that amount.

- No CFAR option. Cancel for any reason coverage lets you cancel a trip for virtually any reason and recoup 50% to 75% of your costs. Most cheap plans don’t offer this as an add-on at all.

- Secondary medical coverage. If your regular health insurance doesn’t cover international care (most US plans don’t), a secondary-only travel policy could leave you negotiating complex cross-border reimbursements at the worst possible time.

- Slow claims processing. Even reputable budget carriers can have sluggish claims departments. Tin Leg, for example, is underwritten by Berkshire Hathaway with an A++ financial rating, but users report mixed experiences with claims speed and processing time.

- Limited evacuation coverage. Remote destinations require high-limit evacuation coverage. A basic plan with $50,000 to $100,000 in evacuation coverage sounds like a lot until you price an emergency air evacuation from Southeast Asia or East Africa, which can run $50,000 to $200,000 on its own.

Experts specifically warn that low-priced plans risk inadequate coverage for medical emergencies abroad. This is the core trade-off: the plan works perfectly fine until something goes seriously wrong.

“Think of cheap travel insurance the way you’d think about a budget spare tire. It’ll get you home from a short drive. But you wouldn’t cross a desert on it.”

The smarter approach is to evaluate your risk level honestly. If you’re taking a 3-day trip to a nearby city with no checked bags and a flexible itinerary, the gaps in a basic plan matter very little. If you’re spending two weeks in a country with expensive healthcare, hiking in remote terrain, or carrying non-refundable deposits worth $3,000 or more, those gaps become real financial exposure. Building strong budget travel habits includes knowing when spending a little more on protection actually saves money overall.

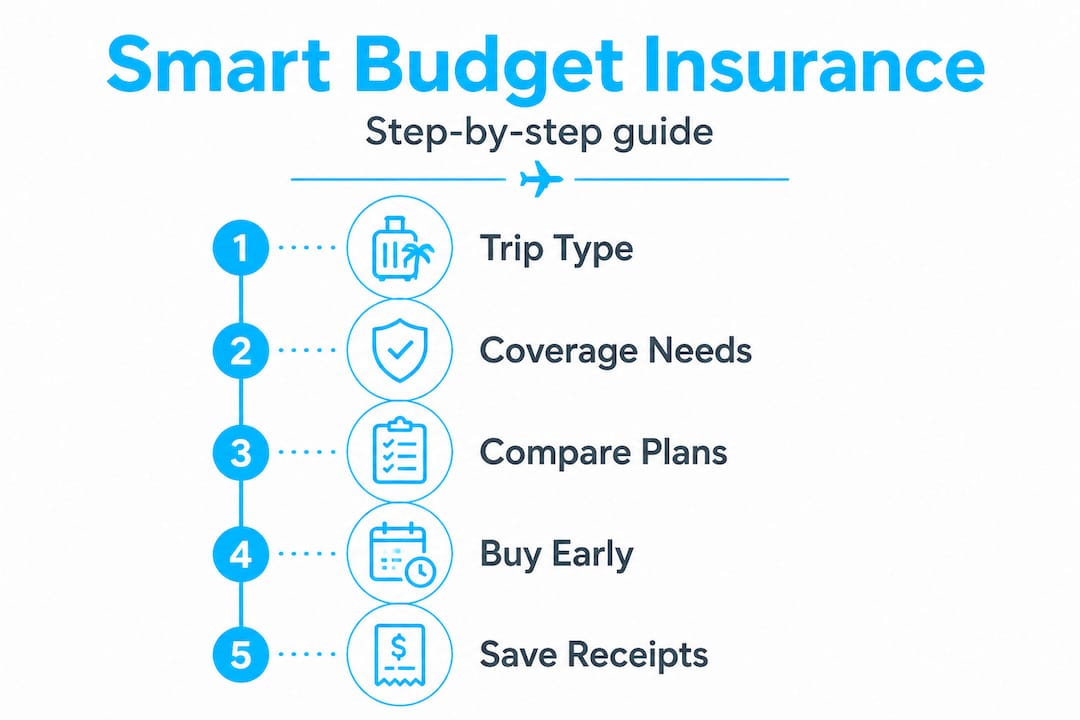

How to choose the right cheap insurance for your trip

Armed with knowledge of the trade-offs, here’s a step-by-step process for matching the most affordable policy to your actual needs.

Step 1: Define your trip type clearly.

Domestic or international? Adventure activities or standard sightseeing? Any pre-existing medical conditions? Remote destination or major city? These answers eliminate most plans immediately and narrow your focus fast.

Step 2: Set your minimum coverage thresholds.

For domestic trips, a basic plan with $50,000 medical coverage often suffices. For international or remote travel, you want at least $250,000 in medical coverage and $500,000 in evacuation coverage. Know your floor before you start comparing prices.

Step 3: Use a comparison site.

Platforms like Squaremouth let you input your trip details and compare dozens of policies side by side in minutes. Filter by coverage level first, then sort by price. This method prevents you from anchoring on the lowest price before confirming the plan actually covers your needs.

Step 4: Buy within 14 to 21 days of your first trip deposit.

Buying early secures pre-existing condition waivers and in many cases unlocks the full scope of trip cancellation benefits. Waiting too long doesn’t just cost you these benefits. It can also leave you unprotected for events that arise before departure.

Step 5: Prepare your documentation in advance.

Claims succeed or fail based on paperwork. Gather receipts for all prepaid trip costs, keep confirmation emails, and document any medical diagnoses or treatment during your trip. Detailed records dramatically increase your chance of a smooth claim.

Here’s a quick reference for matching trip type to plan level:

| Trip type | Recommended minimum plan | Key coverage to confirm |

|---|---|---|

| Domestic weekend trip | Basic ($25 to $43) | Trip cancellation, baggage |

| 1 to 2 week international | Mid-tier ($61 to $90) | $250K medical, evacuation |

| Adventure or remote travel | Comprehensive ($90 to $130+) | High evacuation, sports rider |

| Long trip with large deposits | Comprehensive with CFAR | CFAR add-on, medical primary |

Smart travel budgeting always includes insurance as a line item, not an afterthought. Pairing your policy purchase with your travel checklist ensures you never forget it and that you buy at the right time. If you’re still learning the fundamentals of stretching every dollar on the road, the budget travel planning guide is a solid starting point.

Why focusing only on the lowest price can backfire for travelers

Here’s a perspective that most comparison articles won’t tell you plainly: the cheapest plan on the market is only a good deal if you never need to use it.

That sounds obvious, but it has a real implication. Budget travelers, by definition, often have less financial cushion to absorb unexpected costs. That means the stakes of an inadequate policy are actually higher for budget travelers than for those with more resources. Experts consistently warn that low-priced plans risk leaving travelers with inadequate coverage when medical emergencies strike abroad, and it’s the travelers who can least afford surprise bills who end up most exposed.

We’ve seen this pattern repeatedly. A traveler books the absolute cheapest plan, a $43 basic policy with $50,000 in medical coverage, feels responsible for having insurance, and then faces a $70,000 hospital bill in Thailand after a motorbike accident. The plan pays $50,000. The traveler is on the hook for $20,000. That’s not a worst-case scenario, it’s a realistic one.

The real calculation isn’t “what’s the cheapest plan?” It’s “what’s the cheapest plan that actually covers what could realistically go wrong?” Those are very different questions. Reading exclusions takes 10 minutes. Checking claims reviews on independent platforms takes another 10 minutes. That 20-minute investment can save you thousands.

We believe the smartest budget move is to build your floor first: identify the minimum coverage that protects you from catastrophic loss, then find the cheapest plan that clears that bar. The affordable policy advice we share consistently reflects this philosophy. Price is a filter, not a goal.

Find more ways to save on travel essentials

Getting your insurance sorted is a great start, but real trip savings happen across every booking you make.

At PilotTravelDeals.com, we’ve built a full toolkit for travelers who want to protect their budget without sacrificing experience. Once you’ve locked in the right insurance, you can stretch every remaining dollar by exploring types of travel discounts that apply to flights, accommodations, and activities. Learning the mechanics of using travel comparison sites helps you apply the same comparison mindset to every travel expense, not just insurance. And if airfare is eating the biggest chunk of your budget, our cheap airfare tips guide shows you exactly how to find deals that genuinely move the needle. Smart travel means saving intelligently at every step.

Frequently asked questions

Is it safe to buy the cheapest travel insurance plan?

Cheapest plans are often safe for basic needs but may lack key protections like high medical coverage or cancel-for-any-reason options. Experts warn that low-priced plans risk inadequate coverage for serious medical emergencies abroad.

Who usually gets the lowest travel insurance rates?

Young, healthy travelers with short, domestic trips typically get the lowest rates, but age, trip cost, and destination all impact price significantly. The cheapest plan varies by individual profile, and World Nomads is often favored for travelers under 65 with no age penalty.

What coverage should budget travelers never skip?

Medical and emergency evacuation coverage are critical for most trips, even on a tight budget. Basic plans like Tin Leg suit short domestic trips, but international travel should have at least $250,000 in medical and high evacuation limits.

How can I compare cheap travel insurance plans quickly?

Use travel comparison websites, enter your trip details, and review policy caps and exclusions before buying. Comparison sites like Squaremouth let you filter dozens of policies by coverage level and price in minutes.

Does buying travel insurance early matter?

Yes, buy within 14 to 21 days of booking to secure pre-existing condition waivers and maximize your trip cancellation protection. Waiting too long can permanently lock you out of these benefits regardless of which plan you choose.

Recommended

- 7 Best Websites to Find Cheap Flights for Smart Travelers – PilotTravelDeals.com

- Travel Budgeting – Smart Choices for Affordable Trips – PilotTravelDeals.com

- 7 Smart Steps for an Effective Cheap Travel Checklist – PilotTravelDeals.com

- Why buy travel insurance: protect budget trips 2026 – PilotTravelDeals.com