TL;DR:

- Business travel insurance protects professionals and their employers from high financial risks during work trips. It covers emergencies, trip cancellations, lost equipment, and delays, which can cost thousands or more. Buying coverage promptly after initial trip deposits ensures access to critical benefits and compliance with employer duty of care requirements.

Business travel insurance is defined as specialized coverage that protects professionals and their employers against financial losses from medical emergencies, trip cancellations, lost equipment, and emergency evacuations during work travel. Global business travel spend is projected to exceed $1.64 trillion in 2025, with volumes reaching 86% of 2019 levels. That scale means millions of professionals are exposed to risks that can cost far more than any policy premium. Understanding why business trips need travel insurance starts with knowing exactly what can go wrong, and what it costs when it does.

Why business trips need travel insurance: the core risks

Business travel carries financial exposure that personal trips rarely match. A single canceled multi-leg international trip can result in losses of $4,000 to $12,000 in non-refundable expenses. That figure covers flights, hotels, conference fees, and client commitments that cannot simply be rescheduled without cost.

Medical emergencies are the most severe risk. Emergency medical evacuations from remote regions can exceed $250,000 per case. Without coverage, that bill lands directly on the employer or the traveler.

Flight disruptions compound the problem. Over 21% of flights are delayed and about 1.47% are canceled year to date in 2026. Those numbers translate directly into missed meetings, rebooking fees, and unplanned hotel nights.

Business travelers also carry equipment that personal travelers do not. Laptops, presentation hardware, and proprietary data storage devices represent thousands of dollars in assets. Theft or damage during transit is common, and standard airline liability limits cover only a fraction of replacement costs.

Key risks that business travel insurance addresses:

- Medical emergencies and hospitalization abroad, including ICU care and specialist treatment

- Emergency evacuation to the nearest adequate medical facility or home country

- Trip cancellation and interruption due to illness, natural disaster, or supplier failure

- Lost, stolen, or damaged business equipment including laptops and mobile devices

- Flight delays and missed connections causing downstream financial losses

- Security incidents and civil unrest in high-risk international destinations

Each of these risks is predictable in category, even if unpredictable in timing. That predictability is exactly what makes insurance the rational response.

How does business travel insurance fulfill employer duty of care?

Employers carry a legal and moral obligation to protect employees who travel for work. OSHA’s General Duty Clause and ISO 31030 are the two primary frameworks that document this responsibility. ISO 31030 specifically addresses travel risk management and positions insurance as a documented control mechanism, not an optional benefit.

The compliance trend reflects this shift. 83% of multinational programs made insurance a policy condition in 2024, up from 61% in 2019. That 22-point jump shows that organizations are treating coverage as a baseline requirement, not a perk.

Business travel insurance is a critical component of an employer’s duty of care, providing a documented control mechanism that enables prompt responses to emergencies.

Finance teams see the same logic from a different angle. Travel insurance supports auditable spend, policy enforcement, and minimizes operational disruption. When a traveler files a claim, the documentation trail also satisfies internal audit requirements. That dual function, financial protection plus compliance record, makes insurance a tool for both risk management and budget governance.

The legal stakes are real. Employers who fail to provide adequate coverage for traveling employees face potential liability when incidents occur. Insurance does not just protect the traveler. It protects the organization from claims of negligence.

Benefits of a centralized corporate insurance program:

- Documented duty of care under OSHA and ISO 31030 frameworks

- Audit trails for travel spend and incident response

- Reduced legal exposure in the event of employee injury or illness abroad

- Faster emergency response through insurer assistance networks

- Policy enforcement at the point of booking, reducing coverage gaps

For professionals who want to understand how business travel trends affect risk exposure and costs, the connection between coverage and operational continuity becomes clear quickly.

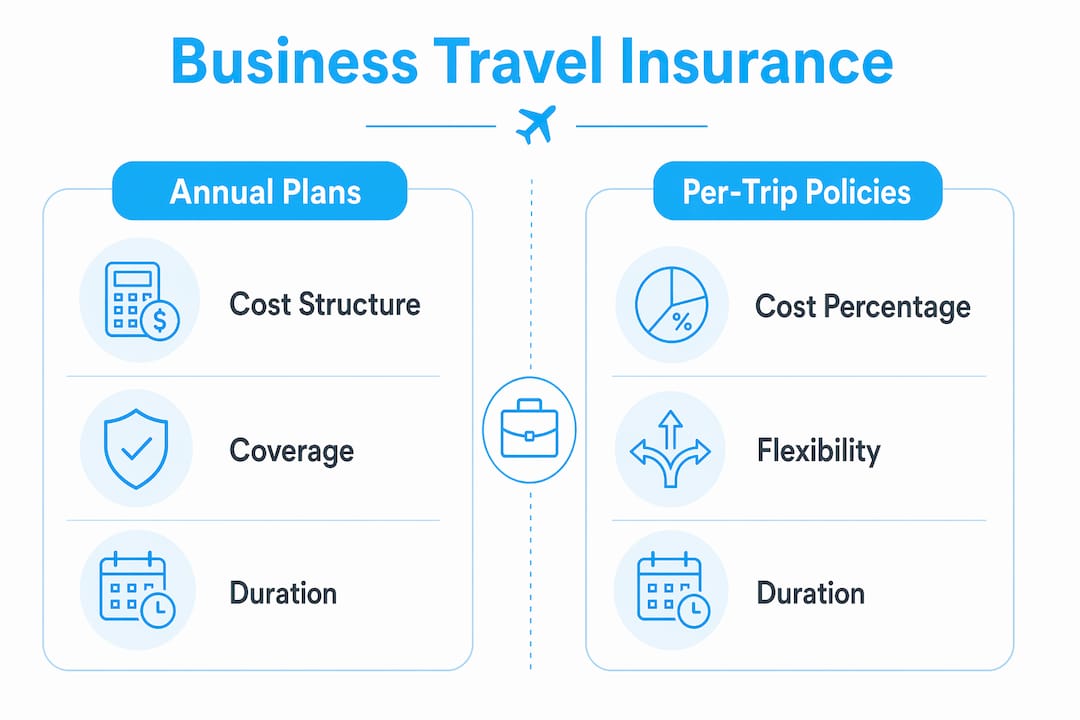

What types of business travel insurance policies are available?

Two main policy structures exist for business travelers: annual corporate multi-trip plans and individual per-trip policies. Annual corporate plans typically cost $300 to $900 per traveler, while individual per-trip policies run 4% to 8% of the total trip cost. For a traveler making four or more trips per year, the annual plan almost always delivers better value.

| Feature | Annual corporate plan | Individual per-trip policy |

|---|---|---|

| Cost structure | $300–$900 per traveler per year | 4%–8% of trip cost |

| Best for | Frequent travelers (4+ trips/year) | Occasional or one-off trips |

| Pre-existing conditions | Often covered under master policy | Usually excluded or requires add-on |

| War and terrorism | Broader coverage via riders | Typically excluded |

| Equipment coverage | Higher limits, customizable | Lower limits, standard |

| Compliance enforcement | Integrated into booking workflow | Requires individual action |

Corporate master policies typically address coverage gaps that standalone retail policies leave open, especially for pre-existing conditions and exclusions for war or terrorism. That gap matters most for travelers going to high-risk regions or those with ongoing health conditions.

Essential coverages to confirm in any business travel policy:

- Emergency medical and hospitalization

- Emergency evacuation and repatriation

- Trip cancellation and interruption

- Lost or delayed baggage and business equipment

- Cancel For Any Reason (CFAR) option

- 24/7 assistance and concierge services

Pro Tip: Review the types of travel insurance available before purchasing. Policies vary significantly in how they define “business equipment” and what dollar limits apply. Confirm the limit covers your actual gear.

Common exclusions to watch for include pre-existing medical conditions without a waiver, self-inflicted injuries, travel to countries under government-issued travel warnings, and losses from unattended baggage. Reading the exclusions section is not optional. It is where most denied claims originate.

What practical steps maximize business travel insurance benefits?

The single most important step is timing. Purchasing insurance immediately after the initial trip deposit unlocks the most valuable benefits, including Cancel For Any Reason coverage and pre-existing condition waivers. Policies bought too late forfeit those protections entirely. This is not a technicality. It is a hard cutoff built into policy terms.

Follow these steps to get full value from business travel coverage:

- Assess trip-specific risks before purchasing. Destination, total non-refundable costs, planned activities, and traveler health history all affect which policy fits best.

- Buy immediately after the first trip payment. The window for time-sensitive benefits like CFAR closes quickly after the initial deposit.

- Book through approved corporate channels. Insurance purchased outside company systems may not qualify for reimbursement or may conflict with the master policy.

- Use digital tracking tools. Real-time traveler tracking lowers incident severity and speeds insurer response when something goes wrong.

- Document everything before departure. Photograph equipment, save receipts, and store policy numbers in a location accessible without your primary device.

- Understand the claims process before you need it. Know the insurer’s emergency line, required documentation, and submission deadlines.

Pro Tip: The decision to buy travel insurance should be based on what you have to lose. For any trip with significant non-refundable costs or international medical exposure, the math almost always favors coverage.

Bundling insurance directly into travel booking workflows reduces claim frequency and improves compliance by enforcing policy at the point of sale. Companies that integrate insurance into their travel management systems see fewer denied claims and faster incident resolution. That is a measurable operational benefit, not just a convenience.

For professionals managing affordable business trip planning, insurance is part of the total cost calculation, not an afterthought.

Key Takeaways

Business travel insurance is a non-negotiable financial and legal safeguard for any professional traveling for work, protecting against costs that can reach hundreds of thousands of dollars.

| Point | Details |

|---|---|

| Medical evacuation costs | A single emergency evacuation can exceed $250,000, making coverage essential for any international trip. |

| Employer legal obligation | OSHA and ISO 31030 require employers to document duty of care, and insurance is the primary control mechanism. |

| Policy timing matters | Buy insurance immediately after the first trip payment to access CFAR and pre-existing condition coverage. |

| Annual vs. per-trip plans | Frequent travelers save more with annual corporate plans ($300–$900) than with per-trip policies (4%–8% of cost). |

| Compliance and audit value | Finance teams use insurance documentation to enforce travel policy and satisfy internal audit requirements. |

The gamble most companies are still taking

I have watched organizations spend six figures on a single medical evacuation that a $600 annual policy would have covered entirely. The math is not complicated. What surprises me is how often the decision to skip coverage gets framed as cost control.

The real cost control argument runs the other direction. A canceled multi-leg international trip costs $4,000 to $12,000 in non-refundable expenses. One hospitalization abroad without coverage can exceed $250,000. No travel budget absorbs that without consequences.

What I find most underappreciated is the compliance angle. ISO 31030 has been in place long enough that “we didn’t know” is no longer a credible defense for an employer facing a negligence claim. The 83% of multinational programs that made insurance a policy condition in 2024 are not being cautious. They are being rational.

The cultural piece matters too. When a company treats insurance as optional, travelers internalize that signal. They buy cheap policies late, skip coverage for short trips, and assume the company will cover gaps. That assumption is wrong, and it is expensive to correct after the fact.

My recommendation is simple: treat insurance as a line item in every trip budget, not a decision point. Build it into the booking workflow. Make it automatic. The travelers who benefit most are the ones who never have to think about it because the system handled it for them.

— Asher

Plan smarter business trips with Pilottraveldeals

Protecting a business trip starts before you book the first flight. Pilottraveldeals brings together hotel deals, cheap airfare options, and travel comparison tools that help business professionals plan trips with full cost visibility from day one.

When you know your total trip costs upfront, choosing the right insurance coverage becomes straightforward. Pilottraveldeals aggregates offers from multiple providers so you can compare flights, hotels, and travel services in one place, giving you the complete picture you need to make informed decisions about coverage and budget. Start your next business trip with a plan that accounts for every dollar at risk.

FAQ

What does business travel insurance typically cover?

Business travel insurance covers medical emergencies, emergency evacuation, trip cancellation and interruption, lost or stolen business equipment, and flight delays. Corporate plans often extend coverage to pre-existing conditions and security incidents that individual policies exclude.

How much does business travel insurance cost?

Annual corporate multi-trip plans cost $300 to $900 per traveler, while individual per-trip policies cost 4% to 8% of the total trip cost. Frequent travelers almost always save money with an annual plan.

When should I buy business travel insurance?

Buy insurance immediately after making the first trip payment. Purchasing early unlocks time-sensitive benefits like Cancel For Any Reason coverage and pre-existing condition waivers that are unavailable if you wait.

Is business travel insurance required by law?

No law universally mandates it, but OSHA’s General Duty Clause and ISO 31030 require employers to document duty of care for traveling employees. Insurance is the primary documented control that satisfies those standards.

Does my employer’s policy cover me, or do I need my own?

Corporate master policies typically cover employees traveling on company business, but coverage limits and exclusions vary. Confirm with your HR or finance team whether the company policy covers your specific trip, destination, and equipment before assuming you are protected.